How segment-level headroom makes shopper segmentation useful in joint business planning

Joint business planning (JBP) is not dead. But the old version – the annual plan that starts with category averages and ends with a long activity list – should be. Retailers and brands still need a place to agree on growth, margins, range, promotions, and channels. What has changed is the standard of evidence behind those choices.

Most joint business plans still begin with category performance. Sales are up or down. Share has shifted. Private labels are applying pressure. Promotions are working, or they are not. Everyone can see the movement.

The harder question is who is moving.

That is where most JBPs stall. Retailers and brands may agree on the size of the prize, but not on the shoppers they are trying to win, defend, or stop losing. Category averages can make that problem look tidy. Segment-level headroom shows the more useful reality: which shoppers matter most, where the value sits, and which actions are worth funding.

1. The average is not the shopper

Category averages show what happened. They do not always show why it happened or who caused it.

A category can look stable while heavy buyers split baskets across retailers. Value can rise while some shoppers trade down and others buy premium packs. A promotion can look successful at the total level while pulling spend from shoppers who would have bought anyway.

That is the risk of planning based on averages: different shopper behavior is treated as a single commercial issue.

Segmentation fixes that only when it forces a decision. A segment has to be large enough to matter, different enough to need its own treatment, and practical enough for teams to act on. If it cannot inform range, price-pack, promotion, channel, shelf, or activation choices, it is not a JBP segment. It is a description.

Panel-based shopper segmentation provides a firmer foundation by starting with measured purchase behavior: what people buy, where they buy it, how often, at what price, and under which promotional conditions. Attitudes still matter, but they work best when they explain behavior rather than replace it.

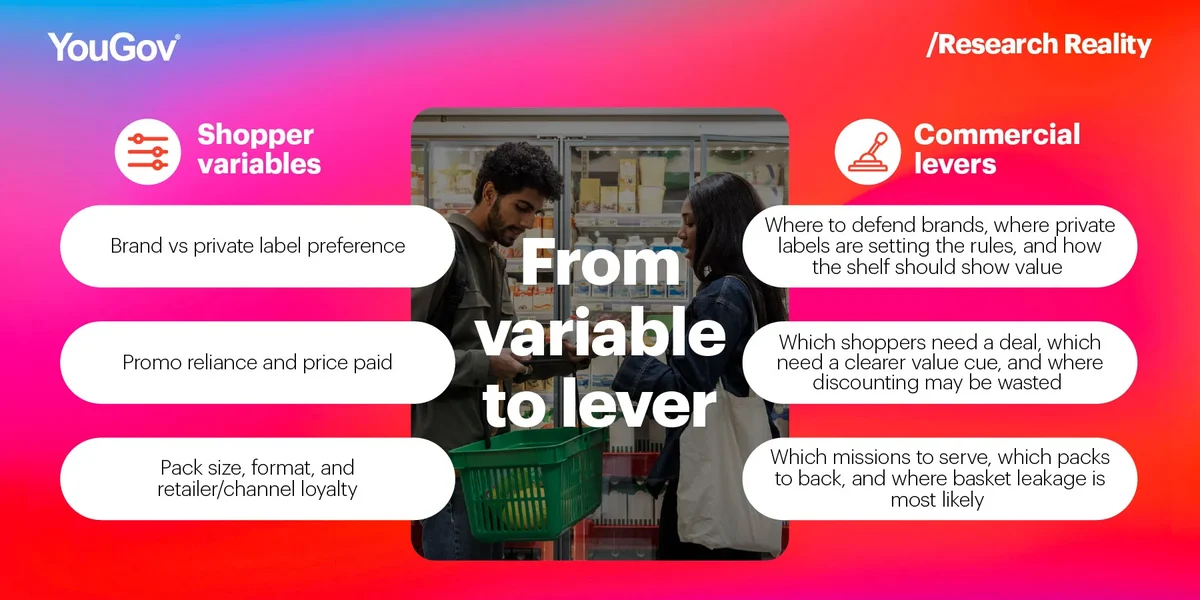

2. Build segments around the levers you can pull

A common mistake is to build a segmentation that is interesting but awkward to use. The chart looks smart. The labels sound plausible. Then the JBP team asks what to do differently on shelf, price, promotion, or channel, and the room goes quiet.

Start with commercial levers, not just shopper traits. For JBP, the best variables are those that point directly to an action:

Other inputs can earn their place – category spend, involvement, sustainability or organic orientation, and selected attitude statements – but every input needs a job. If a variable cannot help the team choose an action, it should not lead the segmentation.

Start broadly to let the data uncover meaningful patterns, then narrow to the variables that make the segments stable, distinct, and commercially useful.

3. Do not turn JBP into a long activity list

The dated version of JBP tries to cover every shopper, every pack, every channel, and every promotional idea. It feels collaborative because everyone gets something in the plan. It rarely creates focus.

Segmentation can fall into the same trap. Nine segments can quickly become nine mini-plans, each with its own message, pack, promo idea, and budget request.

A better JBP asks three questions in order:

- Where is the realistic headroom by segment, retailer, channel, and mission?

- Which shoppers are most worth winning, keeping, or stopping from leaving?

- Which actions can move them without damaging the margin or shifting value in the wrong direction?

The second question is usually the sticking point. Retailers start with what is happening in their own stores. Suppliers start from total category dynamics and brand switching across the market. Both views are valid – but they do not always point to the same answer.

This is where a quantification platform such as YouGov SimIT Web can turn JBP from an annual negotiation into a sharper planning process. Segmentation shows who the shoppers are. Quantification shows where the headroom sits: which segments underperform in a retailer, where competitors over-deliver, and what growth or defense means in value terms.

Then comes the discipline: choose two to four focus segments based on headroom, current value, strategic fit, and cost to win. Some are worth winning now. Some are worth defending. Some are attractive but too expensive. Some are simply not the job for this plan.

4. One plan, two lenses

A good operating model is simple:

Define the segments → size the headroom → choose focus segments → diagnose drivers → agree actions → track movement

The shopper lens explains behavior. The commercial lens sizes the opportunity. Put them together, and the JBP conversation becomes more precise.

Instead of debating which view is “right,” teams can ask a better question: which shopper segment is worth acting on, and what is the shortest list of moves that could shift it?

That shortlist should force decisions on what to back – and what to stop. Which packs deserve space? Which promotions are funding shoppers who do not need funding? Which segments need reassurance rather than discounting? Which channel gaps are worth closing?

The work should not end with a readout. Bring decision-makers in early, then use a working session to turn findings into choices. Set a scorecard for the chosen segments: size, value, retailer share, switching, promotion reliance, and the driver metrics that matter most.

If those measures do not move, the plan should change.

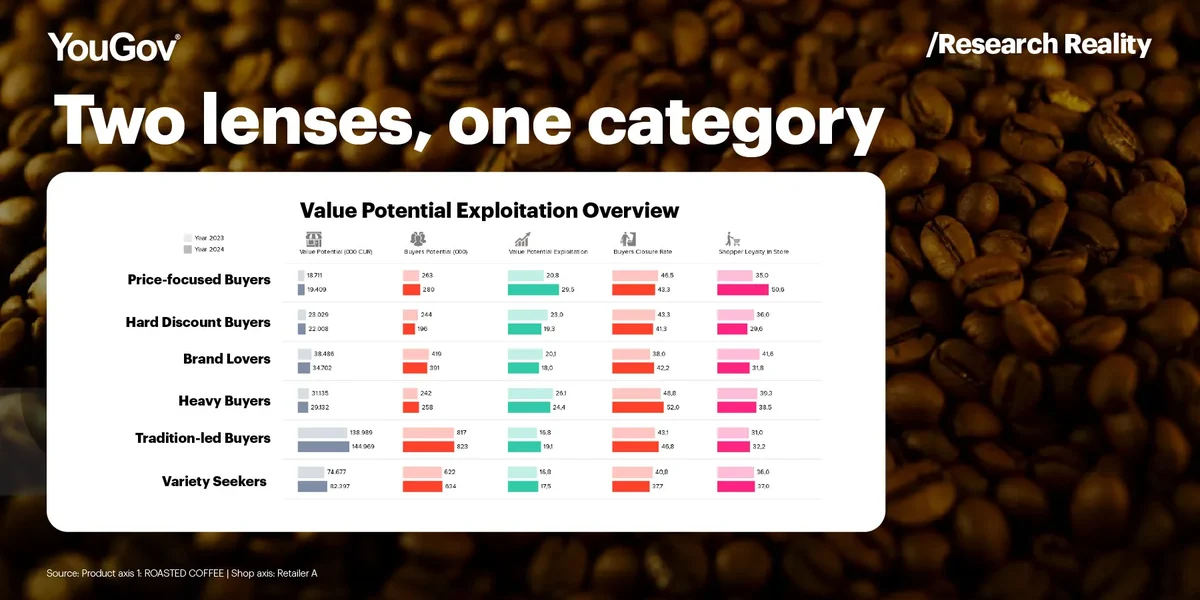

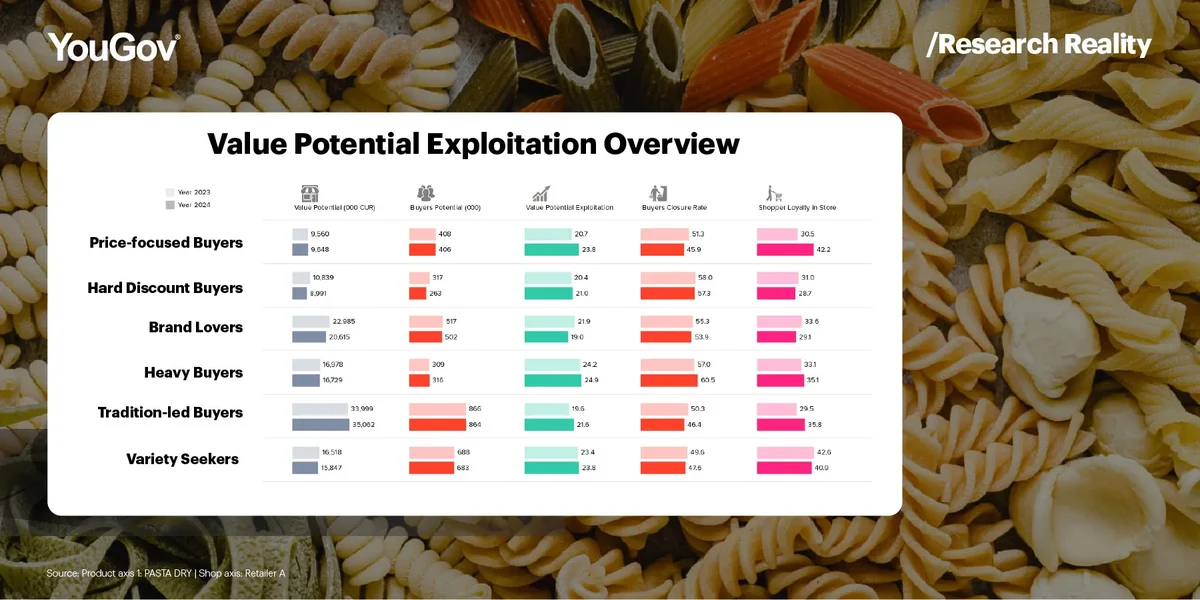

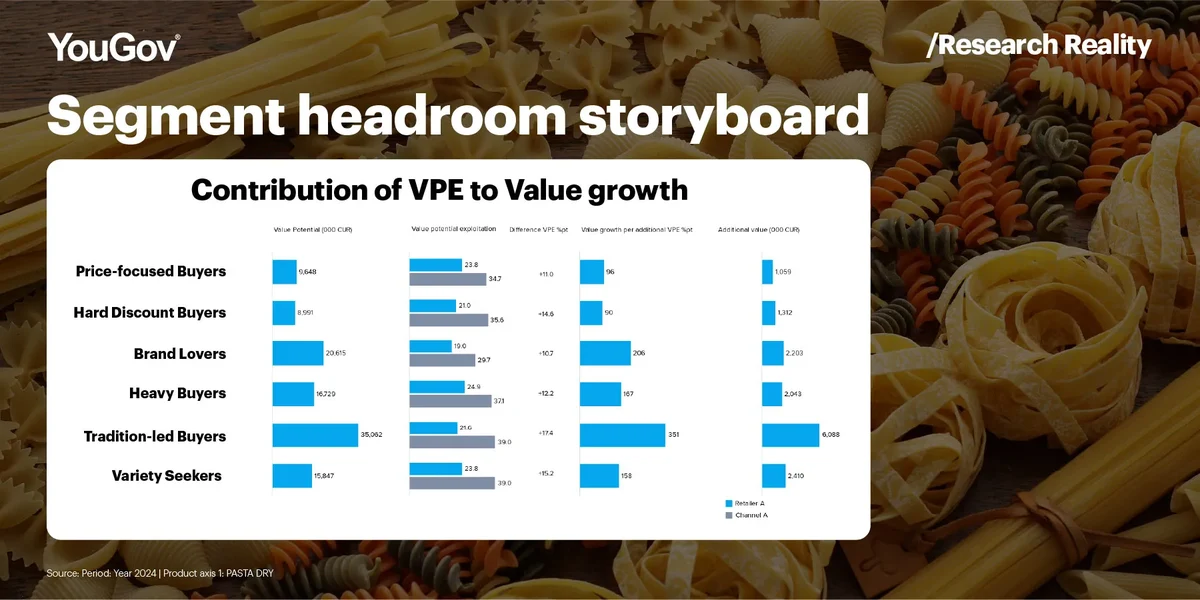

5. Pasta looked stable. The shoppers did not.

A pasta manufacturer and a large grocery retailer were building their JBP for the year ahead. The brief was simple: grow value where growth was realistic, defend share where exposure was high.

At the category level, pasta looked steady. That was almost the problem. The average hid several shopper stories: discount pressure, private label strength, stock-up missions, and shoppers spreading spend across retailers.

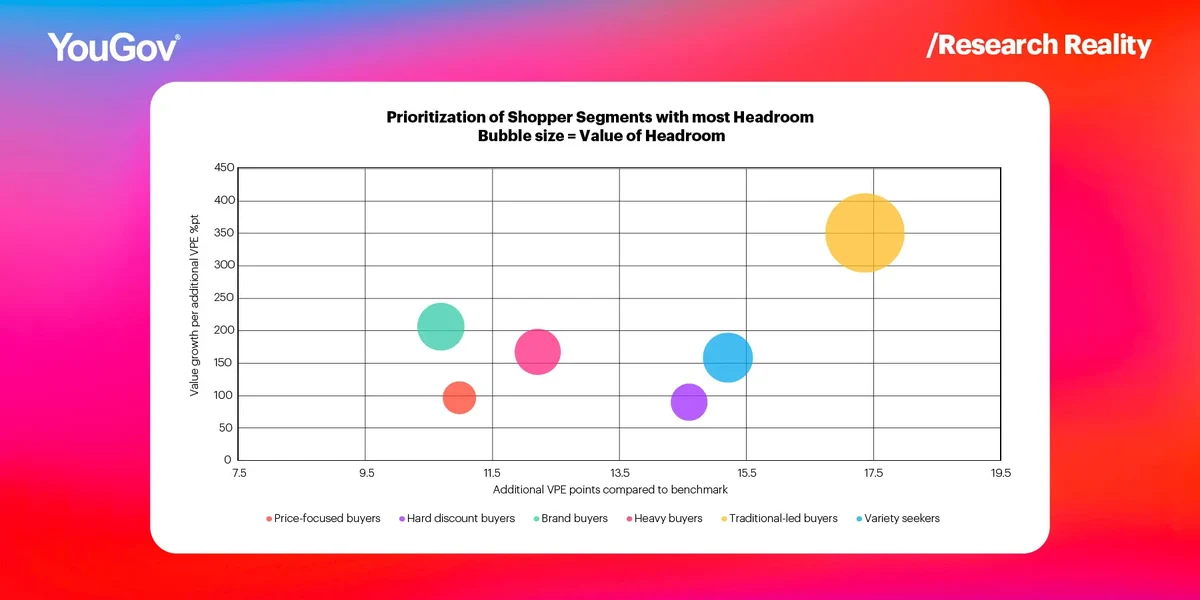

The team started with nine shopper segments, sized the headroom across them, then selected four for decision-making. The useful part was not having nine segments. It used headroom, current value, and cost to win to decide which deserved action.

Two priority segments exposed the problem immediately:

- Heavy buyers drove a large share of value. They shopped across formats and showed stock-up behavior through pack choices and mission structure.

Tradition-led shoppers bought predictably. They were less experimental and relied on familiar cues: format, brand reassurance, and the products they already trusted.

In a standard sales view, “defend share” looked like one job: stay competitive on private label, match promotion mechanics, and protect shelf space.

The segment view split that into two different jobs:

- For heavy buyers, defense meant stopping basket leakage.

The risk was not category exit, but spend shifting across retailers when range, pack size, or value cues worked better for a stock-up mission. The answer was a tighter price-pack ladder and fewer reasons to split the basket. - For tradition-led shoppers, defense meant making the familiar easier to buy.

They did not need more choice or deeper discounts. They needed clarity: a shelf that made trusted options easy to find and avoided confusing trade-offs.

Sizing headroom by segment within the retailer separated what was defendable from what required investment. It also showed which segments justified inclusion in the plan.

The result was a simpler, stronger plan: fewer bets, better funding, and clearer roles for price-pack, shelf, range, and promotion. One smaller segment stayed on the watchlist because the economics did not justify action.

Pasta did not need reinvention. It needed a plan that stopped treating all pasta shoppers as the same.

6. Four moves to make before the next JBP

- Agree on what the segmentation is for

Build around decisions the team can make: price-pack, promotion, format, retailer, channel, and loyalty. - Pick focus segments early

Use actual spend, realistic headroom, strategic fit, and cost to win to choose two to four segments. Define whether each is a growth, defense, or watch priority. - Size the prize, then diagnose drivers

Move beyond who they are to what they are worth – and what would change their behavior. - Track the segments that matter

Use a simple scorecard: segment size, value, share by retailer, switching, promotion reliance, and key drivers.

JBP still has a job to do. But if it starts from category averages, the plan is built on a blurred view of the shopper.

The shift to segment-level decisions is not more complex. It is more disciplined. Fewer assumptions, fewer unfunded priorities, and clearer choices.

And a better answer to the one question every joint plan must face: who are we actually trying to move?

Our segmentation approach is typically panel-led

Most shopper segmentations work best when behavior and attitudes sit together.

YouGov’s panel-led approach combines measured purchase behavior – what people buy, how often, where, and at what price or promotion – with survey inputs on needs, motivations, and barriers. Purchase behavior keeps the segmentation grounded. Attitudes explain why it happens.

The balance changes by situation. Where panel data supports stable segmentation, behavior leads. Where it does not, survey structure leads, supported by behavioral validation.

This is not panel or survey. It is one system: behavior to keep it real, attitudes to keep it useful.