The aviation sector in the Nordics continues to operate under intense scrutiny. From rising operational costs and geopolitical volatility to increasing expectations around service and value, airlines face mounting pressure from both sides of the market.

Yet despite these challenges, demand for air travel remains resilient across Sweden, Denmark, Norway, and Finland. Consumers are still flying – but they are doing so more deliberately, carefully evaluating which airlines they trust and prefer.

Against this backdrop, understanding what drives consideration and satisfaction has become a strategic imperative. The Nordics airline rankings 2026, based on YouGov BrandIndex and Profiles data, provide a comprehensive, data-driven view of how airline brands are performing – and where they are gaining or losing ground.

A competitive landscape shaped by regional dynamics

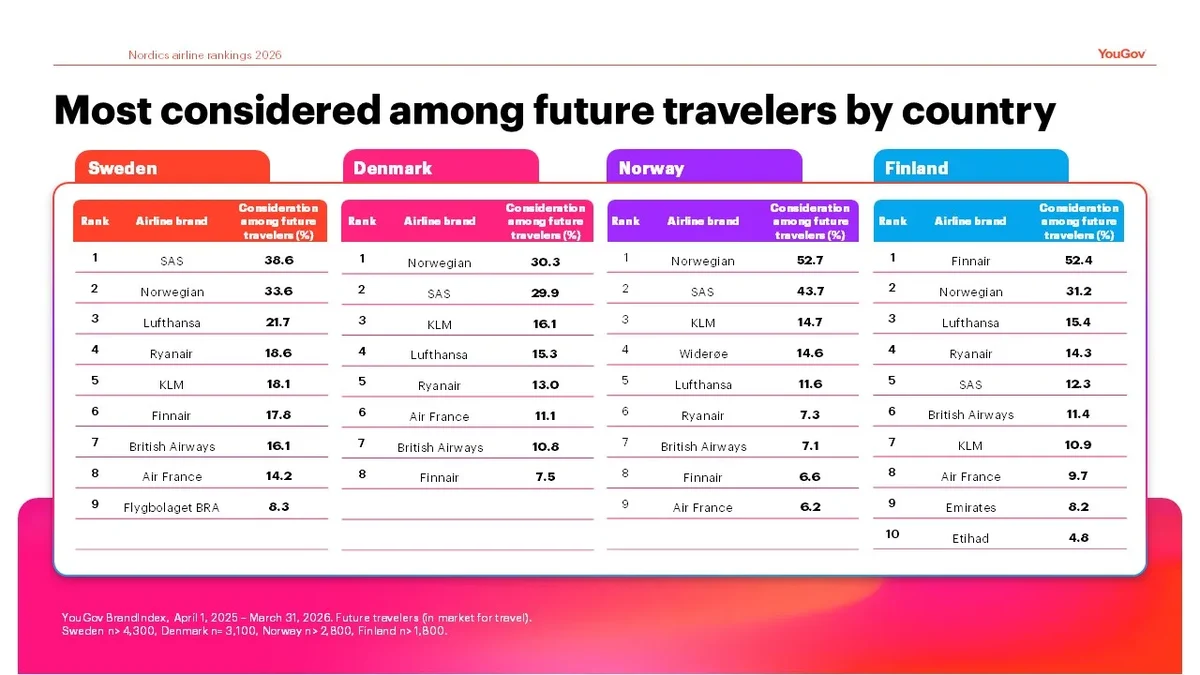

The Nordic aviation market is not uniform. Each country shows distinct patterns in brand preference, shaped by geography, connectivity needs, and national carriers.

In Sweden, SAS leads consideration with 38.6 %, followed by Norwegian at 33.6 %, while in Denmark, Norwegian ranks first at 30.3 %, just ahead of SAS at 29.9 %. Finland stands out as a more concentrated market, where Finnair dominates decisively with 52.4 % consideration, highlighting the strength of national carriers in that market. In Norway, competition is particularly intense, with SAS leading at 43.7 % consideration among future travelers and Norwegian maintaining a strong position as a close competitor.

These variations underline a key regional insight: local relevance and network strength remain critical drivers of consideration in the Nordics. At the same time, international airlines such as Lufthansa, KLM, and British Airways maintain consistent mid- to high-level consideration across markets, reflecting the importance of long-haul connectivity and global brand equity.

Satisfaction: where trust is built – or lost

Across the Nordics, familiar names dominate the satisfaction rankings, broadly mirroring consideration patterns. This alignment suggests that airlines with strong brand equity are, in many cases, also delivering on expectations.

However, improvement trends tell a more nuanced story. SAS shows strong gains in customer satisfaction across multiple markets, including an increase of +8.0 points in Denmark, alongside further improvements of +5.4 points in Sweden and +2.0 points in Norway. Finnair and Lufthansa also record notable increases across markets, with Finnair improving by up to +4.2 points in Sweden and Lufthansa by up to +7.2 points in Finland, underscoring that momentum is not limited to a single carrier but reflects broader competitive shifts.

The implication for airlines is clear: operational delivery, reliability, and service quality are becoming increasingly decisive in sustaining brand strength. In a category where disruptions and delays are highly visible, positive experiences play a critical role in maintaining customer trust and long-term advocacy.

Who are SAS customers?

A closer look at SAS customers reveals a distinct, high-value traveler segment. Compared to the general population, they are significantly more likely to travel frequently, particularly for international leisure trips, and show a stronger affinity for short city breaks. They also tend to be more affluent and more engaged in business travel, highlighting a customer base that combines both personal and professional mobility needs.

Navigating complexity: key takeaways for aviation leaders

The Nordic airline market in 2026 is shaped by a combination of strong competition, evolving customer expectations, and ongoing operational challenges. The data shows that national carriers continue to play a central role in their home markets, while international airlines remain important competitors, particularly on long-haul routes. At the same time, customer satisfaction closely follows consideration levels, indicating that operational delivery and brand perception are strongly linked. Frequent travelers – especially those combining leisure and business travel – stand out as a particularly valuable segment, given their higher travel frequency and stronger engagement with airline brands.

Further insights on brand performance and customer behavior can be found in the full ranking report.

Methode

The rankings in this report are based on nationally representative data. In this report, we have highlighted the top performing brands that are winning over Nordic consumers based on Consideration among future travelers, and Satisfaction among current and former customers. Future travelers are those who are “Somewhat likely”, “Likely” or “Very likely” to purchase a travel in the next 12 months.

Consideration score is based on the question: ‘When you are in the market next to purchase a trip, from which of the following would you consider purchasing?’ For the Satisfaction rankings, respondents answered the question: “Of which of the following brands/companies would you say that you are a Satisfied/Dissatisfied Customer?”

A minimum base size of 300 (n) is required. To qualify as top ranked, brands have held tracked scores for at least 6 months (183 days). To qualify as top improvers, brands have held tracked scores for at least 18 months (548 days).

Scores have been rounded to a single decimal place. For improvers, brands are ranked based on their change in scores. In cases where the change in score is the same between two brands, the current scores are used as a secondary metric to determine their ranking.

The customer profiles in this report are powered by YouGov Profiles – an ever-growing source of consumer data, with 2+ million data variables from YouGov’s 30+ million global panelists. The data used in this report was accessed via Profiles+ Sweden, 2026-05-10.

Throughout the report, unless otherwise noted, each generation is defined as: Gen Z (1997 or later), Millennial (1981-1996), Gen X (1965-1980) and Baby Boomers+ (Pre-1964).