Standing at the beginning of 2026, the view looks daunting for shoppers and industry players as last year left a hard inheritance: massive pressure on costs, high fiscal unpredictability that rewrote market dynamics, a struggling shopper seeking more value for their money and retail consolidation shifting even more negotiation power into retailer hands. But let’s take it one by one.

Understanding inflection points

We’ve already grown used in recent years to instability. The year 2025 came after a 2024 marked by an artificial calm, created by the situation on the political stage with multiple rounds of elections, which – sustainable or not – meant also higher incomes for the Romanian shopper that were allocated more towards leisure activities and hospitality. The idea of stability and of a functioning economy was “sold” very well, meanwhile Romania was “building” the highest budget deficit in European Union [8.6% in 2024]. Then, the first turning point came along with the Presidential election annulment and signs of shopper spending withdrawal appeared. The second inflection point, a harsher wake-up call, followed mid-year 2025 when a series of fiscal austerity measures hit the country and… the wallets. To put the cherry on top, the National Institute of Statistics just announced that Romanian economy is in technical recession, having two consecutive quarters with negative development, while budget deficit remained high at 7.65% in 2025.

In this context, there should be no surprise that Consumer Confidence Index started to go once again down in January 2026 [after a slight stabilization in Q4 2025] and that consumers are under pressure. Looking at the results of latest YouGov Shopper Behavior Change Survey, nearly half of Romanian household [45%] are barely making ends meet. This represents a significant increase [8.2pp] since Spring 2025, showing that more people are moving away from a 'comfortable' or 'neutral' financial state and into financial health crisis.

At home, once again a safe haven?

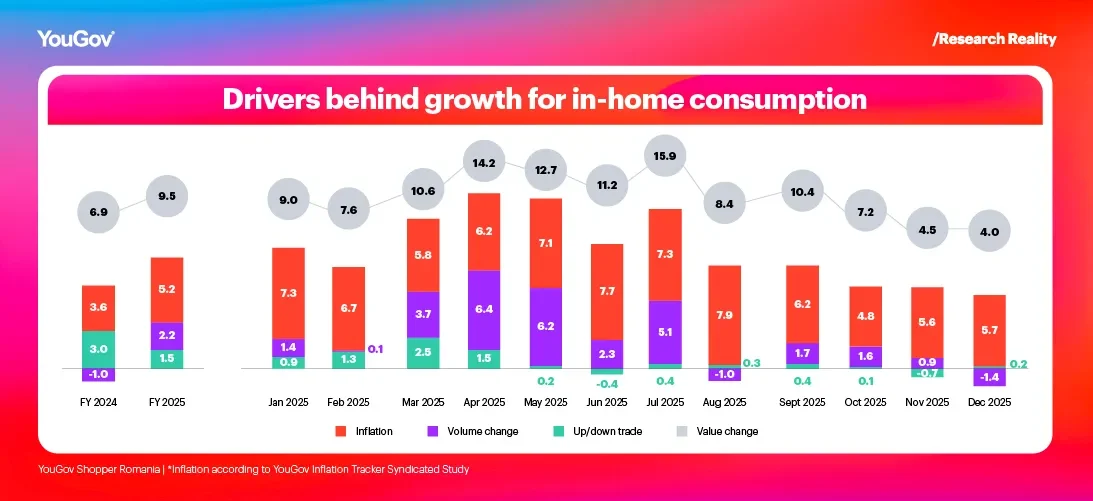

The same YouGov Shopper Behavior Change Survey shows that high prices for out-of-home activities are more alarming for Romanians than high prices for daily necessities, but even so 7 out of 10 declare that they will spend less in general on everyday goods. And we already see a shift in occasions, with a contraction for out-of-home and only partial volumes “recuperated” in-home. Here, at total 2025 level, FMCG value saw an almost double digit increase [9.5% vs. PY], with a mix of inflation [5.2%], volume increase [+2.2% vs. PY] and up-trading [+1.5% vs. PY].

Even so, as the year progressed, the shopper appetite to buy more or premium is visibly declined, culminating in December when – despite the holiday’s excitement – growth was almost entirely driven by inflation.

With budget pressure, more coping strategies come into play. “Checking prices”, “searching or waiting for promo” and “do more home cooking” practices are at the top of the shoppers list. Nevertheless, the strongest growth during 2025 was seen by the action of shifting from premium to more affordable brands.

YouGov Shopper Panel Romania data also shows that promo sales had once again boosted in second part of the year [+2pp vs. PY, up to 25.7% from total FMCG] after a slow start in H1 [only +0.7pp vs. PY]. Also, private label segment which has been overshadowed by branded segment in past years [due to promo investment], now shows signs of recovery adding 0.5pp in H2 2025 vs. PY, but overall, 2025 remaining flat at 24.4%.

Almost 3 out 10 categories battle a higher wave of inflation

Zooming at macro-baskets level, Fresh Food registered a contraction of 0.8pp vs. PY but continues to cover 30.3% of the spending at home. Food [21.6%] and Beverages [20.2%] follow importance wise, both adding 0.4pp in value share vs. PY, managing to outgrow the industry pace. Still, the most dynamic segment is Baby Food & Care.

Against inflation, not all categories were equal. 28% of them experienced a higher rate than FMCG average while volume increases within these were the smallest [only 51% of them positive]. Here, we find categories such as fresh fruits, water, biscuits sweet & salted, carbonated soft drinks, yoghurt, edible oil, milk or chocolate cream, just to give some examples. At the other end of the spectrum, for just above 4 out 10 categories, inflation was below industry average, while the rest [31%] were in line with total FMCG level.

Another fact one can notice when looking at categories affected by volume decreases, is that for majority of them, the main factor behind was penetration. These categories were dropped from the basket and there is also a common thread: many of this cluster are in the indulgence zone [e.g. chocolate countlines, popcorn, peanuts in glaze, instant hot chocolate, bath foam, perfumed candles etc...].

As for shopping missions, they also reflect the need for more control over spendings, with Cherry Picking [1-3 categories, Promo Share >50%;] and Large Stock-Up [12+ categories] strengthening from trips perspective [+0.5pp vs. PY and, respectively, +0.4pp vs. PY]. The second also gained most in value share [+1pp vs. PY, up to 31.6%] in detriment of Stock-Up [4-11 categories].

Major shifts on the retail scene

Last year started and ended with a bang, plus a mid-year interlude. First, came the announcement that the 1.3 billion Euros mega transaction through which Ahold Delhaize was taking over Profi Rom Food is final, with the condition coming from Competition Council that 87 stores to be sold [now part of local chain Annabella]. Even so, Ahold Delhaize more than doubled its store footprint in Romania, playing under 3 banners [Mega Image, Shop&Go and Profi], and adding 3 billion euros in net sales for the group.

Then came June with the news that Schwartz Group, owner of Kaufland and Lidl, plans to acquire the majority stake [70%] in local player La Cocos. The transaction is also seen as a “done deal”, after some months of negotiation with the Competition Council that raised some conditions accepted now by Schwartz Group [e.g. keeping the same business model, network expansion etc].

Then came October 2025 with the first signs of a potential divestment of French group Carrefour in Romania, as part of a broader strategy to optimize its international portfolio. The press reporting was officially confirmed just at the begging of 2026, with a clear front runner in the discussion: the owners of Romania’s largest home improvement retail chain, Dedeman.

While the acquisitions from local entrepreneurs [Annabella, Dedeman] are seen as success stories, especially by shoppers, the withdrawal of a big player such as Carrefour is also a sign of a sector that lately has struggled under new legislation and taxes [e.g. taxes on turnover rather than on profit, caps on commercial mark-ups, increasing asset taxes, high labor taxation, lack of fiscal predictability].

Drawing the line and despite these challenges, other players continue to invest, and the overall number of stores opened in 2025 surpassed that of PY. But even from this perspective, the balance is in favor of franchise concepts such as Froo, Simply by Auchan and La Doi Pasi, accounting for more than half of new openings. Profi Loco and Penny were the two others at the lead of the expansion top.

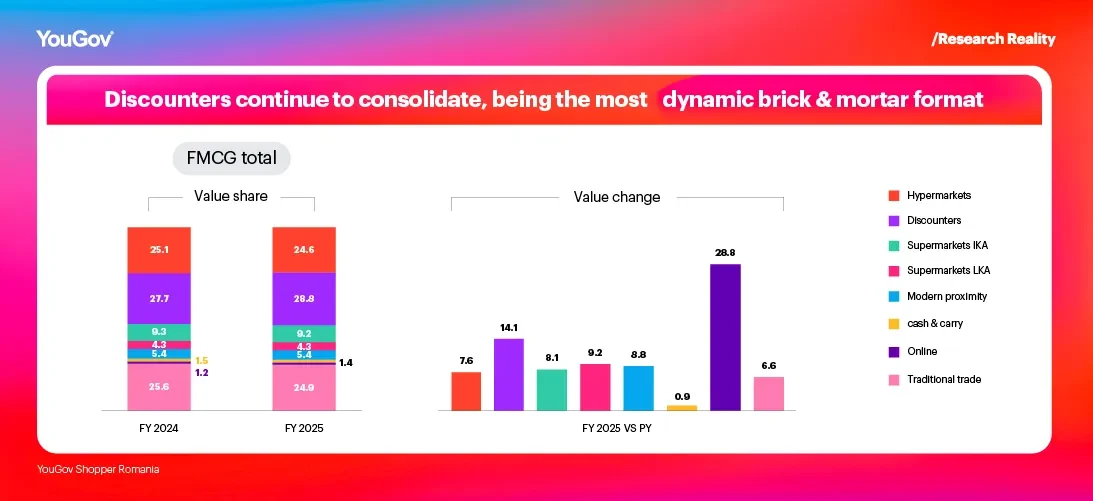

For at home, Discounters continue to thrive and consolidate, now standing at 28.8% market share, with Lidl as leader [20.5%] and, on the other hand, with Penny more dynamic than most players [+14.9% vs. PY in abs. terms]. Value in this channel was attracted from all other formats [except Online], but especially from Traditional Trade and Hypermarkets, which were also the two channels losing most share.

Market consolidation also continued, with top 10 banners now covering 65.5%, while from retail groups perspective 4 – Ahold Delhaize, Auchan Group, Carrefour Group and Schwartz Group – account for almost 60% of at home sales.

Another aspect that was reconfirmed in 2025 is related to the role of expansion. Seen many years as the main pillar for growth, it is now a “pawn” in the bigger scheme of the loyalty game. The decrease in importance is also confirmed by the fact that, despite new openings, only one player – Penny – managed to attract new buyers. When it comes to loyalty or, plainly said, how much of the shopper’s wallet is retain by each retailer, here Lidl is first once again [22.8%, +1pp vs. PY], while Mega Image and Profi Loco advanced most after Lidl.

Can anybody say what’s really coming next?

While the Government talks about the technical recession as an expected effect of last year’s measures, which will be short lived with a recovery starting mid-year; plenty of market analysts say that this is not a given, especially if a more profound decision will be further postponed [e.g. administrative reform and the streamlining of the state apparatus].

For the moment, official sources from European Commission to International Monetary Fund and National Bank of Romania, converge towards the same image: 2026 a year of transition, with modest growth [~1%], declining inflation [3.6-6%], but still a very large deficit [6.2%]. Of course, critical months lay ahead.

As for the grocery retail and FMCG industry, caution seems to be the key principle for 2026. Many are revising their investment plans, prioritizing operational efficiency, accelerating digitalization and automation, while portfolio wise, focus is on optimization and customer loyalty.

Methodology: YouGov Shopper Panel is based on continuously collected data and rolling surveys on 6,000 households representative for the total population in Romania.

YouGov Shopper Intelligence, Consumer Panel Services [formerly part of the GfK group through 2023], offers access to a wealth of expertise and quality consumer panel data. We help the world’s most recognized FMCG & Retail brands to deliver superior customer experiences at every stage of the shopper journey. Learn more about Shopper Panel.