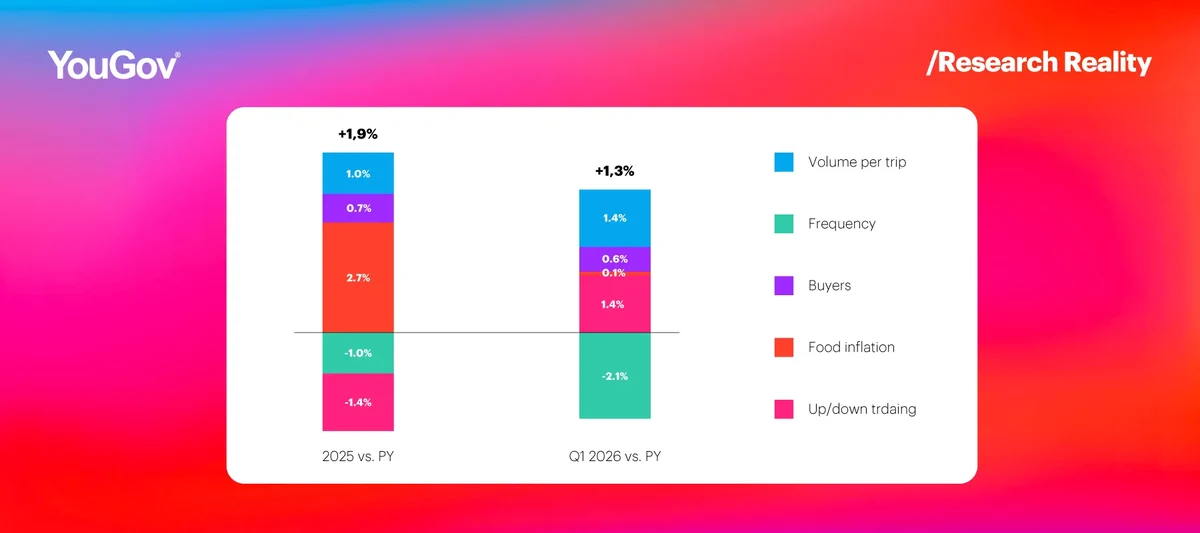

In the first quarter of 2026, the growth of the Belgian FMCG has slowed, it is +1,3% versus last year, making a small shift form the +1,9% seen in FY 2025.

KPIs

While food inflation was the primary driver of value growth in 2025, it has for now moderated to nearly zero. As a result, households no longer needed to actively seek cheaper alternatives, leading to an uptrading effect of +1,4%. Unlikely, this trend is not driven by a shift from PL to A-Brands. Instead, PL OM is the biggest winner this quarter.

This quarter, frequency puts downward pressure on value growth. Although higher volume per trip partially offsets this decline, it is not sufficient to fully compensate.

The drop in frequency by 2,1% is not unexpected, as the quarter was affected by a negative calendar effect, particularly in March, due to fewer Saturdays.

(Price) War between Retailers

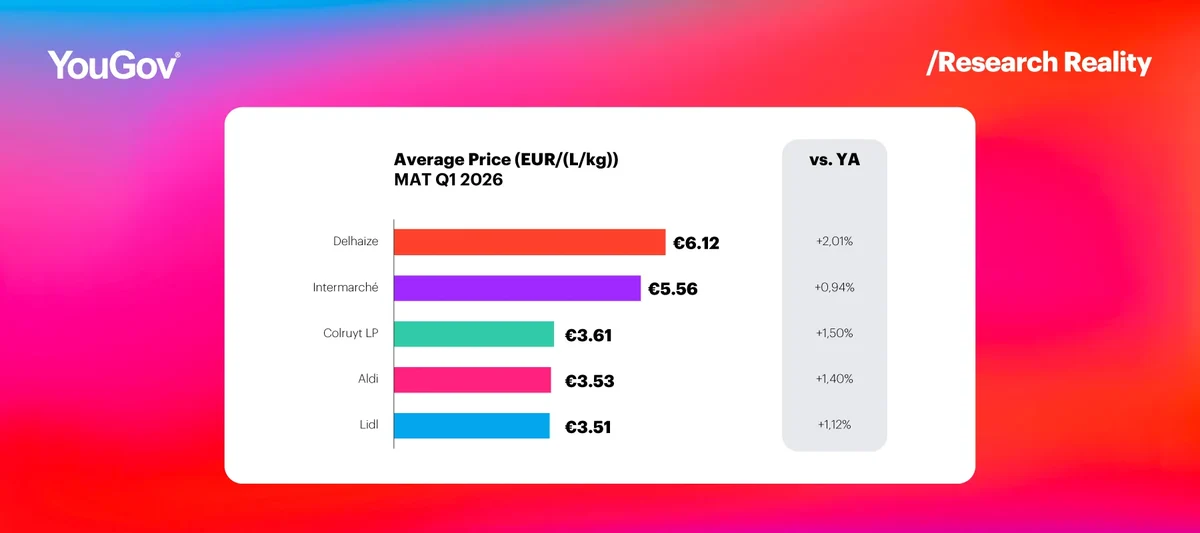

In Q1, the price war between retailers intensified and became a hot topic in the Belgian retail landscape. Delhaize launched in the beginning of January an advertising campaign comparing the prices of a selection of basic products across the largest supermarket chains, even claiming to be cheaper than hard discounter Lidl.

This campaign triggered strong reactions from competitors: Colruyt, Lidl and Intermarché responded with their own comparisons emphasizing that they remain the cheaper option. Could the intensified price war have enabled households to afford more premium options, thereby contributing to the uptrading effect observed this quarter?

On MAT basis, Lidl records the lowest average price paid per household, confirming its position as the cheapest retailer overall.

Hypermarkets: the end of an era

Looking at the hypermarkets channel in Belgium, the long term trend leaves no room for doubt about the future of this retail concept, even if sometimes the short term shows a different picture.

In the year 2000, hypermarkets had a value share of 17,4% on total FMCG. 25 years later, the hypermarket channel ended 2025 with a value share of only 3,9%. In 2000, there were 4 banners of hypermarkets in BE, now just one survived.

Hypermarkets were the store format that brought us the consumption society with their unique USP of unbeatable prices & everything under the same roof (and they still do in emerging markets). But the times have changed over the last 65 years, since the opening of the first Hypermarket in 1961, and their USP has faded.

Looking Forward

Looking ahead, several key questions will shape the market’s evolution. One of the most pressing is if food inflation accelerates again toward a 2% level, potentially triggering downtrading behaviour, too. At the same time, it is yet to be seen how the share balance between A-Brands and Private Label will evolve.

Stay tuned to find out!