How is the FMCG market in Poland currently developing?

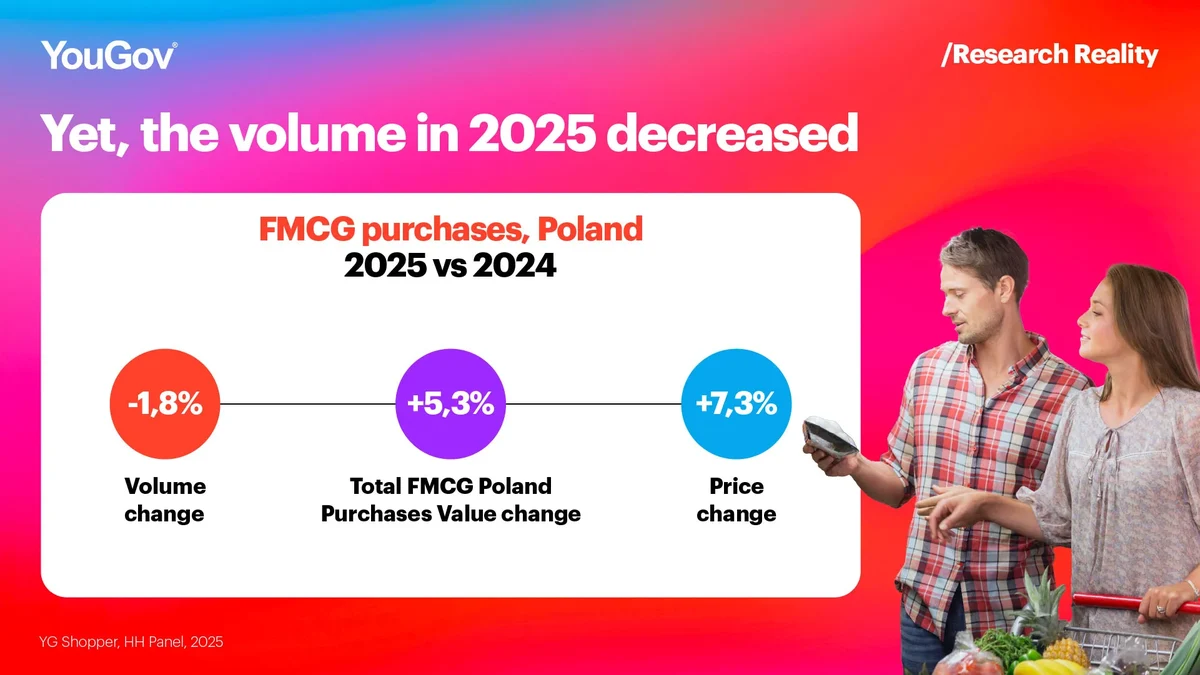

Polish consumers entered 2026 with greater financial optimism than the average European, but their purchasing decisions remain cautious. According to YouGov, in 2025 the Polish FMCG market declined in volume by 1.8% year-on-year, while its value increased by 5.3%, which translated into an additional PLN 14.5 billion.

Behind these numbers, there are deeper and long-lasting structural changes. The share of households facing serious financial difficulties is decreasing, and 42% of consumers now say they feel financially stable. At the same time, nearly 30% still struggle to make ends meet, showing a clear polarization. In practice, this means two different attitudes: some consumers feel more comfortable spending, while others stay highly focused on controlling their budgets.

Poles love promotions

Our data clearly shows that Poland remains a market moderately driven by promotions. In 2025, more than 33% of FMCG purchases were made during promotional offers, and their importance continues to grow. Although this may seem like a high result, in terms of the share of promotional purchases Poland ranks only 10th among 16 European countries included in the YouGov study. The ranking is led by the Czech Republic, where promotions account for 56% of purchases, while Belgium ranks last with 19%.

The role of discount stores is also gradually increasing. Their market share has exceeded 44%. Small chain-format stores and drugstores also remain in good condition and are recording a significant growth rate.

New growth drivers

In 2025, the positive market dynamics were mainly driven by categories related to freshness and convenience. Among the segments that contributed additional volume to shopping baskets were fresh meat, fruit and natural yogurts, kefir, ready meals, functional beverages, iced tea, and fresh fruit. On the other hand, volume declines were recorded in categories such as detergents, alcohol, dog food, and sliced cold cuts.

Less randomness, more control

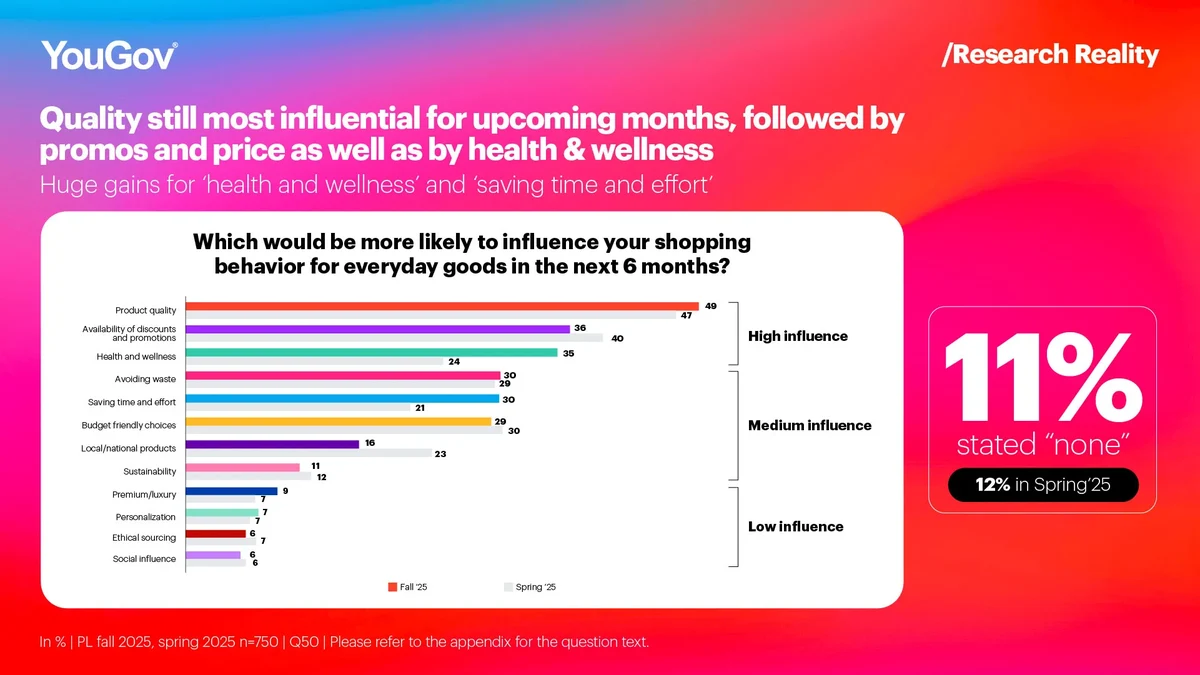

According to the Behavior Change report, in the coming months the biggest influence on consumers’ purchasing decisions will be quality, promotions and price, as well as health and well-being. Meanwhile, the Trend Galaxy report shows that the key need supporting consumer trends will be security and control. Already today, 97% of households say that this factor has a moderate or strong influence on their purchasing decisions (including 57% who say the influence is strong).

This is where the most dynamic and lasting changes are happening. Consumers are clearly moving towards healthier and more conscious choices – high-protein products are now very common (around 83% penetration), and functional drinks are growing fast. At the same time, reduced-sugar products have reached around 60% penetration. Bio, eco, and local products are now almost standard (around 99% of households), showing that the market is maturing. This is not a short-term trend, but a long-term shift in how people think about food and health.

In 2026, further growth is expected in segments such as functional food and beverages, bio, eco, vegan and organic products, gluten-free food, reduced-sugar products, and high-protein products. According to our experts, this is not a temporary trend but a clear shift in the way people think about food and health. Consumers are becoming increasingly conscious of what they put in their shopping baskets, and the FMCG market will need to keep up with this change.

Methodology:

YouGov Shopper Poland is built on continuously collected data from 8,000 households, representing the country’s total population.

YouGov Shopper offers access to a wealth of expertise and quality consumer panel data. We help the world’s most recognized FMCG & Retail brands to deliver superior customer experiences at every stage of the shopper journey. Learn more about YouGov Shopper.