When Shoppers Don’t Shop More—But Spend Differently

FMCG Shopping in Transition: Frequency, Missions, and Channel Shifts

Households’ FMCG expenditures in the Czech Republic have increased year on year by nearly 4%, driven primarily by a higher average price paid. This is reflected in higher spending per trip, reaching 360 CZK on average per shopping basket.

As anticipated, shopping frequency has stabilized at 296 trips per household. While in the past we observed a higher willingness to shop more frequently as a reaction to inflation, this trend has now leveled off. If no major disruptions occur, shopping frequency is likely to return to its pre-crisis trajectory and gradually decline.

Decoding Shopping Missions and Basket Structures

Why is frequency so important? Each shopping trip represents a touchpoint for both brands and retailers with their shoppers. It is therefore crucial to understand this pool of evolving opportunities.

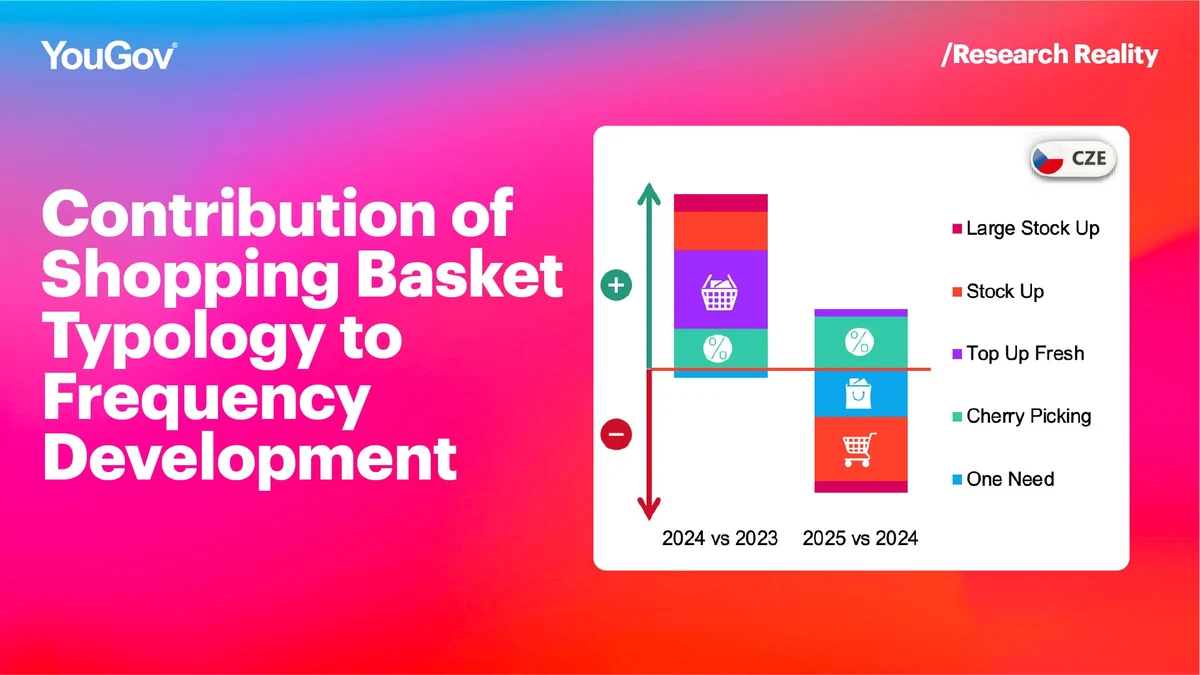

Not all trips are the same. Shoppers do not buy individual brands and categories in isolation; instead, they purchase them together across various shopping missions. Each mission reflects the fulfillment of different needs, with each need represented by a specific product category. We can therefore distinguish between small one-need baskets (or cherry-picking trips), medium-sized top-up fresh baskets—predominantly focused on fresh food—and stock-up or large stock-up trips.

Although overall shopping frequency is not changing dramatically, its structure is. In 2024, more mid-sized top-up fresh baskets were realized. In 2025, as frequency stabilized, we are seeing fewer stock-up trips and fewer one-need baskets. These shifts pose significant challenges for retailers. Revenue dynamics differ substantially depending on whether growth is driven by smaller or larger baskets. Therefore, understanding how these changes affect retailers—as well as the categories and brands purchased alongside each mission—is crucial for overall success.

Shopping Channel Evolution: The Growing Role of Online

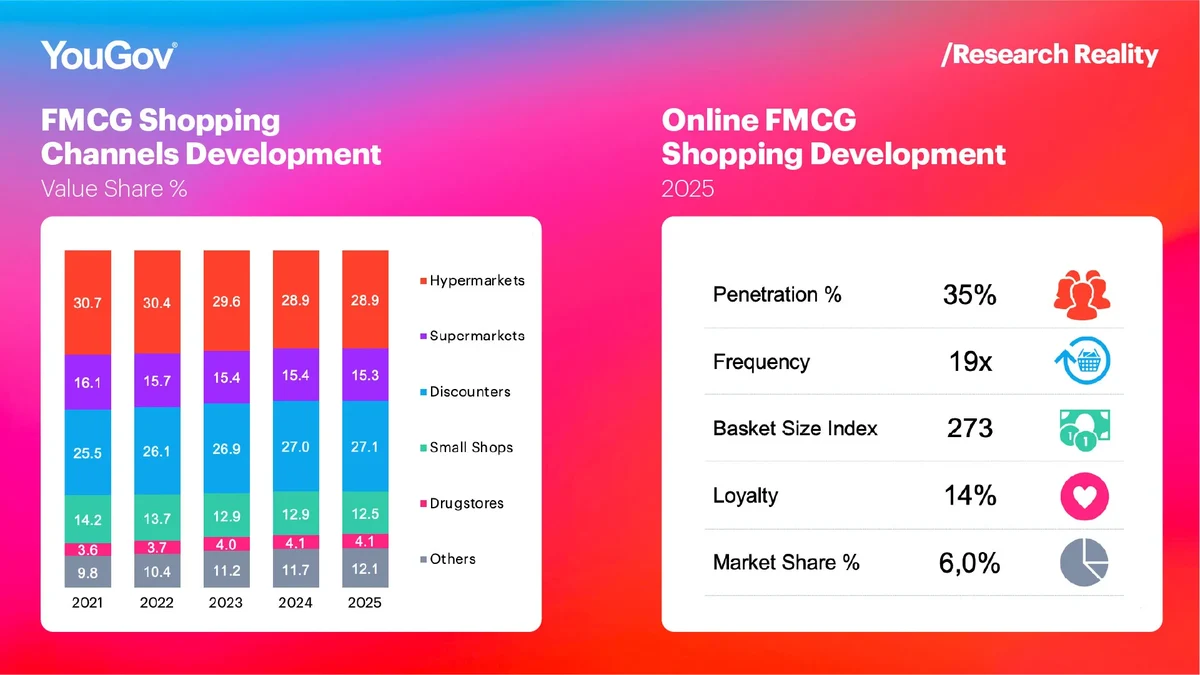

All FMCG shopping channels have maintained relatively stable positions, with the exception of small shops, where changes have been driven by specialized stores. Online FMCG shopping is the fastest-growing channel in the Czech Republic, already accounting for 6% of total household grocery expenditure.

Among households that shop online, this channel plays an even more significant role, with 14% of their total FMCG spend allocated to online shopping. Shopper penetration has remained relatively stable; however, more frequent trips and higher-value baskets (2.7× higher than average) have driven the growth of FMCG e-commerce.

The largest trips and stock-up missions are particularly prominent online, resulting in net value gains across all key channels, especially supermarkets and hypermarkets.

For stationary FMCG retail, success will depend on navigating evolving shopping missions while competing with online FMCG, which is increasingly capturing shopper spend through more shopping trips as well as significantly higher-value baskets.

Methodology:

YouGov Shopper Czech Republic is built on continuously collected data from 4,000 households, representing the country’s total population.

YouGov Shopper offers access to a wealth of expertise and quality consumer panel data. We help the world’s most recognized FMCG & Retail brands to deliver superior customer experiences at every stage of the shopper journey. Learn more about YouGov Shopper.