Unpacking inflation, demand shifts and the real drivers of FMCG performance

Bulgaria’s FMCG market growth in FY25 is higher than FY24 - in both value and volume — despite persistent price pressure and a more cautious shopper. The key shift is not that shoppers have stopped spending, but how they spend: they plan more, compare more, and lean into promotions and value choices to keep control of their baskets.

Resilient shoppers, still under pressure

Ahead of euro adoption in Jan ’26, YouGov Shopper ran its 6th edition of “Behavior Change” survey (n=750, Nov/Dec ’25). Only 1 in 3 households feel financially insecure, yet budget concerns remain the #1 issue and are rising and worries about high prices for daily goods remain above EU-15 levels.

This mindset is translating into action. Shoppers increasingly state they will check prices, search for / wait for promotions, and keep the total basket amount low—alongside everyday tactics like using leftovers / cutting waste and home cooking.

At the same time, this is not a story of pure restriction. Bulgarians claim buying what one likes, preferably on promo, with a good quality and no barrier towards private label.

The result is a shopper who is firmly in control: not “switching off” purchases but actively optimizing it across channels, brands, pack sizes and promotional timing.

Growth is real — but the engine matters

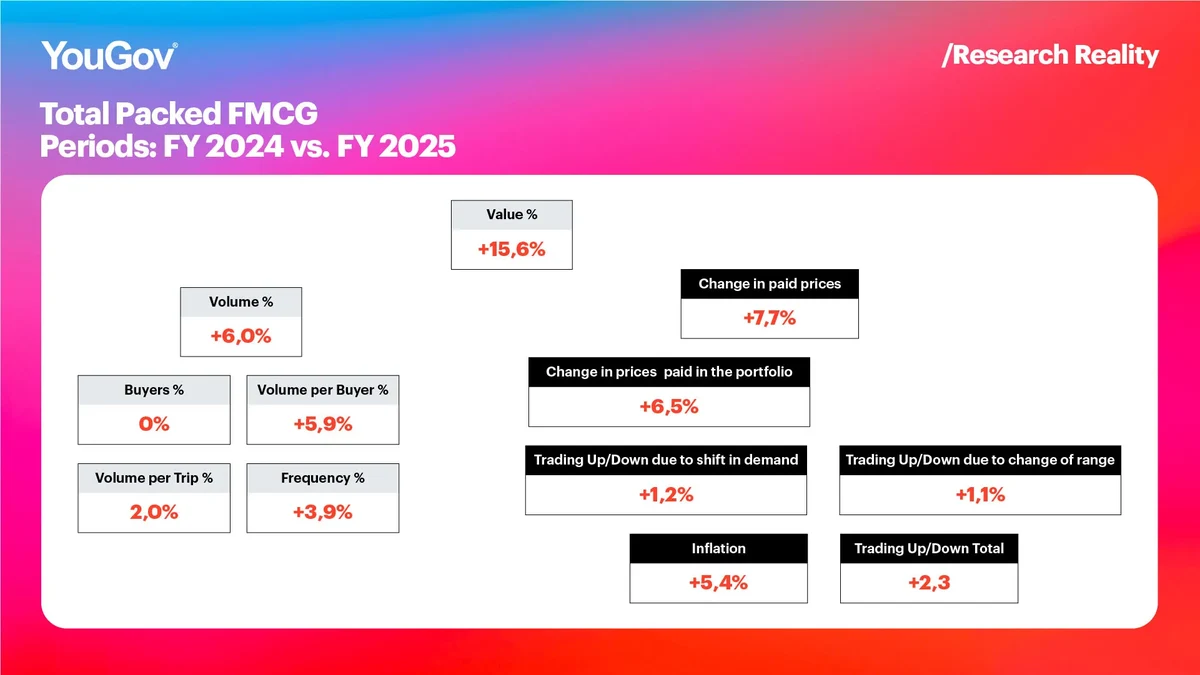

The Consumer Panel data shows Packed FMCG (250 categories) is up in both value and volume in FY25 vs. FY24. Households shop more frequently and buy more per trip.

Yet when we follow the trail using YouGov Price Pulse, the picture becomes clearer. The average paid price increased by 7.7%, and most of that increase was driven by inflation alone. Pure inflation accounts for 5.4 percentage points of the change, while shifts in shopper choice and assortment explain a much smaller 2.3 percentage points.

In other words, value growth exists — but it is still largely price‑led, not demand‑led.

This distinction matters. Inflation‑led growth tends to be more fragile. Shopper tolerance has limits, competitors can undercut quickly, and promotions can absorb price increases before they translate into sustainable net revenue. When prices rise faster than real demand, pricing discipline becomes a strategic necessity rather than a hygiene factor.

Inflation-led growth increases the importance of managing the price, promotional dependency and elasticity across the portfolio.

Two strategies are playing out — in parallel

Nowhere is this dynamic more visible than in the contrast between private label and branded products.

- Private label inflation: +4.3% vs brands +5.7%

- Private label volume growth: +15.16% vs brands +3.49% (≈5x faster)

- Trading Up/Down Index (demand): brands +2.90% vs private label +1.28%

Price Pulse shows that private label inflation in FY25 was significantly lower than brand inflation. At the same time, private label volume grew around five times faster than manufacturer brands. This points clearly to affordability and switching as the primary drivers of private label growth.

And yet, brands tell a different story. While brand volume growth remains modest, the Trading Up/Down Index shows that demand within brands is shifting upward more strongly than within private label. Simply put, the shoppers who stay with brands are trading up — choosing higher value propositions, stronger benefits, and more premium variants.

Private labels are winning volume through affordability and switching, while brands are more likely to sustain value through premium mix within remaining branded demand.

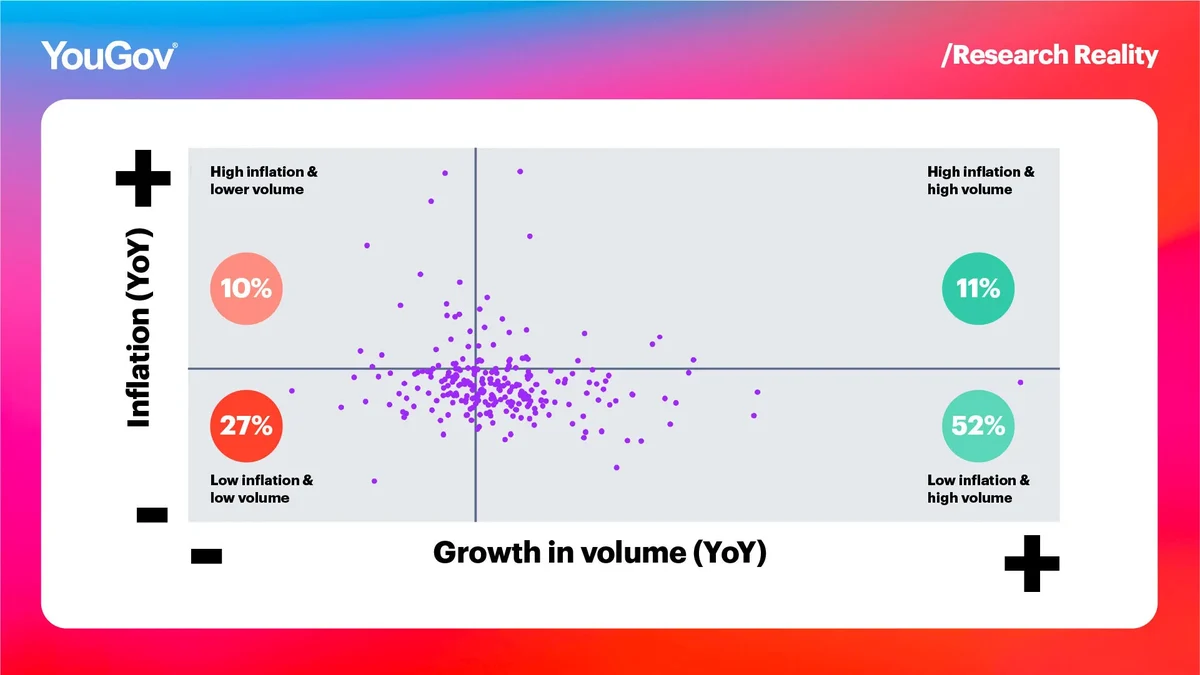

Categories are not “born equal”: the inflation–volume rule breaks often

It would be tempting to assume that inflation automatically leads to declining volumes and vise versa. The data says otherwise. Across 250 FMCG categories, that rule holds for about 62%. But for the remaining 38%, inflation and volume do not move in expected directions.

Some categories grow volume despite high inflation. Others struggle even when inflation is relatively low. A clear illustration comes from coffee. Both roasted beans and roasted ground coffee experienced some of the highest inflation levels year on year. Yet roasted beans continued to grow in volume, supported by buyer recruitment and stable up‑trading, while roasted ground coffee lost penetration and showed signs of down‑trading.

Inflation matters, but it is not destiny. Penetration dynamics, price‑pack architecture, promotional intensity and elasticity determine outcomes category by category.

Turning insight into action

This is where measurement becomes a competitive advantage. In an environment where inflation still dominates price movements and shoppers continuously adapt, tracking reality - not assumptions - is critical.

YouGov Price Check enables manufacturers and retailers to monitor inflation, demand shifts and assortment dynamics based on what shoppers actually pay, not just list prices. It shows which price increases stick, where promotions erode net price, and how assortment changes influence value.

At the same time, YouGov Choice helps teams move from observation to optimisation. By simulating pricing and promotional strategies before they go to market, brands and retailers can understand elasticity, avoid unproductive discounting, and design price ladders that protect volume while sustaining margin.

The takeaway

FMCG growth in Bulgaria is real — but it is built on a careful balance. Shoppers are resilient, but vigilant. Inflation still does most of the work, but tolerance is finite. The winners will be those who continuously track price reality, understand demand dynamics, and actively shape pricing and promotions rather than reacting to them.

The question is no longer whether to manage price — but how well you do it.

Methodology: YouGov Shopper Bulgara is based on continuously collected data and rolling surveys on 2500 households representative for the total population of the country.

YouGov Shopper offers access to a wealth of expertise and quality consumer panel data. We help the world’s most recognized FMCG & Retail brands to deliver superior customer experiences at every stage of the shopper journey.